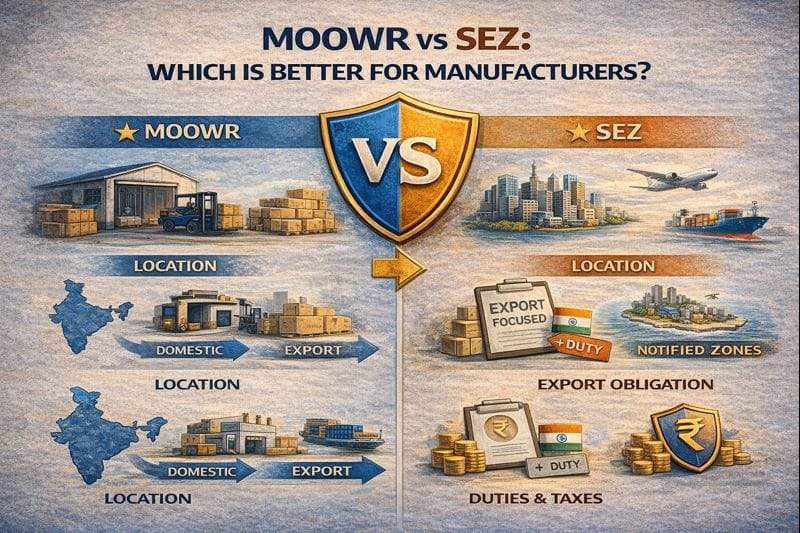

The MOOWR vs SEZ comparison has changed materially, and most published guidance has not caught up. MOOWR is a duty-deferment scheme under Sections 58 and 65 of the Customs Act, 1962, operable at any location in India, with no export obligation. SEZ is a designated zone under the SEZ Act, 2005, treated as outside the customs territory.

The decisive point for a new manufacturer is that the SEZ income tax holiday is no longer available, and SEZ units must maintain positive Net Foreign Exchange. MOOWR imposes neither.

Section 10AA of the Income Tax Act granted a 15-year phased tax holiday on export profits. It carries a sunset clause. The deduction is available only to units that commenced manufacture or production before 1 April 2021.

A new SEZ unit set up today cannot claim it. Units established before the cut-off continue to claim within their remaining window, but any comparison that lists income tax benefits as a live SEZ advantage for new investment is out of date. Do not build it into your return calculation.

This is the constraint that shapes SEZ operations. An SEZ unit must achieve positive Net Foreign Exchange earnings, assessed cumulatively over a five-year block. Failing NFE at the end of the block can lead to duty recovery and cancellation of the Letter of Approval.

MOOWR has no NFE requirement, no export obligation, and no performance review of that kind. A MOOWR unit may sell one hundred per cent of its output domestically.

A MOOWR unit can be established anywhere in India, including by converting an existing factory or warehouse into a private bonded facility. There is no geographic restriction and no minimum investment.

An SEZ unit must sit inside a notified zone, which frequently means relocation or greenfield construction. Setup cost and lead time are correspondingly higher.

The mechanisms differ in kind, not just degree:

MOOWR requires digital accounts furnished monthly to the bond officer under Regulation 17, a triple duty bond under Section 59, and a warehouse keeper with customs experience. Physical customs control was removed.

SEZ units operate under a Development Commissioner, file through the SEZ Online portal, undergo periodic performance review, and must track NFE cumulatively. Oversight is heavier and more institutional.

Choose MOOWR if you sell substantially into the domestic market, want to use an existing facility, import capital goods and inputs, and cannot commit to sustained export performance. The trade-off is forfeiting RoDTEP and drawback.

Choose SEZ if you are a large, export-driven operation able to maintain positive NFE across a five-year block, and the zero-rated procurement and duty-free import outweigh the setup cost and locational constraint. Do not choose it for the income tax holiday, which is closed to new units.

Neither side of the MOOWR vs SEZ choice is permanently fixed. MOOWR now carries a proviso to Section 65(1), inserted by the Finance (No.2) Act, 2024, allowing the Central Government to exclude classes of goods and operations by notification. Section 65A provides for withdrawal of the IGST exemption, effective date not yet notified by CBIC.

The SEZ framework itself is under review, with the proposed DESH Bill contemplating a shift beyond a purely export-led model. Neither scheme should be treated as permanently fixed.

At JPARKS INDIA, we run the MOOWR vs SEZ comparison on your actual numbers: capital goods value, input import volume, export ratio, domestic sales forecast, and the RoDTEP forfeiture. We flag the Section 10AA position honestly rather than quoting lapsed benefits. Having served 500+ importers and exporters since 2018, we keep the decision quantitative. Learn more about our MOOWR scheme services or book a free consultation.

It depends on export intensity. MOOWR suits domestic-focused manufacturers wanting flexibility and no export obligation. SEZ suits large exporters able to maintain positive NFE. The SEZ income tax holiday is closed to new units.

No. The Section 10AA deduction is available only to units that commenced manufacture or production before 1 April 2021. Units set up after that date cannot claim it.

An SEZ unit must achieve positive Net Foreign Exchange earnings, assessed cumulatively over a five-year block. Negative NFE can trigger duty recovery and cancellation of the Letter of Approval.

No. MOOWR imposes neither. A MOOWR unit may sell one hundred per cent of its output into the domestic market, paying the deferred duty on the imported inputs contained in those goods.

Yes. A MOOWR facility can be established at any location, including by converting an existing factory. An SEZ unit must be located within a notified zone.

EXCELLENTTrustindex verifies that the original source of the review is Google. Very prompt and reliable service by Rahul Kolge and his team. Exceptional and happy experience.Posted on GoogleTrustindex verifies that the original source of the review is Google. Had a really good experience with JParks India. Rahul sir helped me a lot with my import work and were always active and responsive. Whatever documents or guidance was needed, they handled everything smoothly and explained things clearly. Felt stress-free throughout the process. Very helpful team, definitely recommend them if you’re doing import or export.Posted on GoogleTrustindex verifies that the original source of the review is Google. Very nice people, get the work done in a very short time.Posted on GoogleTrustindex verifies that the original source of the review is Google. Excellent & Prompt services in all Import Export matters. Great to work with youPosted on GoogleTrustindex verifies that the original source of the review is Google. It was a great experience having work with you.Posted on GoogleTrustindex verifies that the original source of the review is Google. "Outstanding professiona services, efficient, and gets things done incredibly fast. Highly recommended for anyone needing reliable and prompt assistancePosted on GoogleTrustindex verifies that the original source of the review is Google. excellent servicePosted on GoogleTrustindex verifies that the original source of the review is Google. JParks Team is Super helpful! Thanks to Rahul and team!Posted on GoogleTrustindex verifies that the original source of the review is Google. Good and personal service for import export codePosted on GoogleTrustindex verifies that the original source of the review is Google. Had a really good experience with JParks India. Rahul sir helped me a lot with my import work and were always active and responsive. Whatever documents or guidance was needed, they handled everything smoothly and explained things clearly. Felt stress-free throughout the process. Very helpful team, definitely recommend them if you’re doing import or export.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

We use cookies to run this site, measure traffic, and track our ads. Essential cookies are always on. Accept all, reject non-essential, or set your preferences.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Google Tag Manager simplifies the management of marketing tags on your website without code changes.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a web analytics service that tracks and reports website traffic. It collects anonymized data on how visitors use the site to help us understand and improve performance.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Google Ads is an advertising service used to deliver and measure ads, including conversion tracking for our campaigns.

Service URL: policies.google.com (opens in a new window)

Google Maps is a web mapping service providing satellite imagery, real-time navigation, and location-based information.

Service URL: policies.google.com (opens in a new window)

You can find more information in our Cookie Policy and .