MOOWR manufacturing operations are far broader than most guidance suggests. Section 65 of the Customs Act, 1962 permits manufacture and other operations in relation to warehoused goods, and it contains no words of qualification or limitation regarding the nature of the goods or the activity involved.

That is not an interpretation. It is the express holding of the Delhi High Court in ACME Heergarh Powertech, which rejected the argument that Section 65 is confined to a particular genre of goods or manufacturing.

Section 65 uses the word goods, which includes all kinds of goods: raw materials, components, consumables, and capital goods. The phrase manufacturing process or other operations is deliberately wide.

The Court held that reading Section 65 to cover only capital goods that themselves undergo a process of manufacture, or that are consumed in the resultant product, would place an extremely narrow construction on the statutory language. Neither Section 61 nor Section 65 incorporates an implied exclusion for any particular industry.

The expression in relation to, used in Section 65, conveys comprehensiveness. It suggests a causal link between the imported goods and the manufacturing activity undertaken in the warehouse.

Capital goods need not transform themselves. They need only be connected to, or contribute to, the manufacturing process or operations in the warehouse. This is why machinery installed and used inside a bonded facility qualifies, even though the machine itself never becomes part of the finished goods.

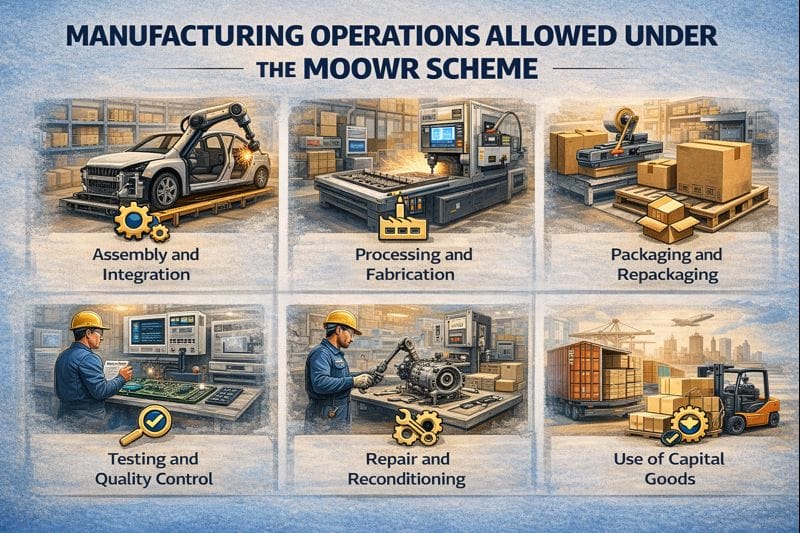

In practice, MOOWR manufacturing operations span the full range of value addition:

Here is the limit that genuinely bites when planning MOOWR manufacturing operations. Job work is permitted, but only inputs may be sent out to a job worker’s premises.

Imported capital goods cannot be shifted to a job worker. Only tools, moulds, drawings, and similar items may be provided. The main machinery must stay in the bonded facility. Capital goods may, however, be sent outside for repair with the permission of the bond officer.

The application under Regulation 4 requires the applicant to inform the input-output norms for raw materials and final products, and to report any revision. SION norms do not apply, so you declare your own.

Operating outside the declared scope is a breach of licence conditions and can attract cancellation under Section 58B. The point is not that customs pre-approves a narrow list, but that you must operate within what you declared and report changes.

This changes the picture for MOOWR manufacturing operations going forward. A proviso to Section 65(1), inserted by the Finance (No.2) Act, 2024 and administered by CBIC, empowers the Central Government to notify manufacturing processes and other operations, in relation to a class of goods, that shall not be permitted in a MOOWR unit.

Before that amendment, the breadth of Section 65 was the point, as the Delhi High Court confirmed. Exclusion can now occur by notification. A separate notification effective 17 December 2024 restricts warehousing where electricity is the resultant good.

Duty is payable on the portion of imported inputs attributable to scrap or refuse arising from operations. If scrap is destroyed, no duty is payable. If it is exported, duty is calculated as if the goods were originally imported in that form, on the transaction value of the scrap.

All such activity must be recorded in the prescribed accounts and reflected in the monthly return.

At JPARKS INDIA, we scope MOOWR operations correctly at the application stage, declare accurate input-output norms, structure job work within the permitted boundary, and keep the declared activity aligned with what actually happens on the floor. Where the 2024 proviso creates exposure for your class of goods, we say so. Having served 500+ importers and exporters since 2018, we keep bonded manufacturing compliant. Learn more about our MOOWR scheme services or book a free consultation.

Section 65 contains no words of limitation on the nature of goods or the activity. Assembly, processing, fabrication, packaging, testing, repair, and reconditioning are all undertaken, alongside use of imported capital goods.

The Delhi High Court in ACME Heergarh Powertech held that Section 65 cannot be read as restricted to a particular genre of goods. However, since 2024 the Central Government may exclude classes of goods and operations by notification.

No. Only inputs may be sent for job work. Imported capital goods cannot be shifted to a job worker’s premises, though tools, moulds, and drawings may be. Capital goods can be sent out for repair with the bond officer’s permission.

It conveys a causal link. Capital goods need not transform themselves, only contribute to or be connected with the manufacturing process or operations carried out in the warehouse.

Yes, on the portion of imported inputs attributable to the scrap. If the scrap is destroyed, no duty is payable. If exported, duty is computed on the transaction value of the scrap as if originally imported in that form.

EXCELLENTTrustindex verifies that the original source of the review is Google. Very prompt and reliable service by Rahul Kolge and his team. Exceptional and happy experience.Posted on GoogleTrustindex verifies that the original source of the review is Google. Had a really good experience with JParks India. Rahul sir helped me a lot with my import work and were always active and responsive. Whatever documents or guidance was needed, they handled everything smoothly and explained things clearly. Felt stress-free throughout the process. Very helpful team, definitely recommend them if you’re doing import or export.Posted on GoogleTrustindex verifies that the original source of the review is Google. Very nice people, get the work done in a very short time.Posted on GoogleTrustindex verifies that the original source of the review is Google. Excellent & Prompt services in all Import Export matters. Great to work with youPosted on GoogleTrustindex verifies that the original source of the review is Google. It was a great experience having work with you.Posted on GoogleTrustindex verifies that the original source of the review is Google. "Outstanding professiona services, efficient, and gets things done incredibly fast. Highly recommended for anyone needing reliable and prompt assistancePosted on GoogleTrustindex verifies that the original source of the review is Google. excellent servicePosted on GoogleTrustindex verifies that the original source of the review is Google. JParks Team is Super helpful! Thanks to Rahul and team!Posted on GoogleTrustindex verifies that the original source of the review is Google. Good and personal service for import export codePosted on GoogleTrustindex verifies that the original source of the review is Google. Had a really good experience with JParks India. Rahul sir helped me a lot with my import work and were always active and responsive. Whatever documents or guidance was needed, they handled everything smoothly and explained things clearly. Felt stress-free throughout the process. Very helpful team, definitely recommend them if you’re doing import or export.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

We use cookies to run this site, measure traffic, and track our ads. Essential cookies are always on. Accept all, reject non-essential, or set your preferences.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Google Tag Manager simplifies the management of marketing tags on your website without code changes.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a web analytics service that tracks and reports website traffic. It collects anonymized data on how visitors use the site to help us understand and improve performance.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Google Ads is an advertising service used to deliver and measure ads, including conversion tracking for our campaigns.

Service URL: policies.google.com (opens in a new window)

Google Maps is a web mapping service providing satellite imagery, real-time navigation, and location-based information.

Service URL: policies.google.com (opens in a new window)

You can find more information in our Cookie Policy and .